Table of Contents

- Introduction

- Understanding Voluntary Payment Under Section 74

- Procedure for Voluntary Payment Using Form GST DRC 03

- Voluntary Payment Before a Show Cause Notice: Penalty Benefits

- Tax Liability Under Section 74

- Penalties and Interest Under Section 74

- Show Cause Notice (SCN) Under Section 74

- Consequences of Skipping Payment Under Section 74

- Common Defences Against a Section 74 Show Cause Notice

- Section 73 vs Section 74 vs Section 74A — Spot the Difference Cheat Sheet

- Conclusion

The Goods and Services Tax (GST) revolutionized India’s taxation system in 2017. It aimed to simplify and unify the country’s complex tax structure. Within this framework, Section 74 of the Central Goods and Services Tax (CGST) Act plays a crucial role in addressing tax evasion cases.

Section 74 of the Central Goods and Services Tax (CGST) Act gives businesses that have short‑paid or wrongly claimed GST a narrow window to put things right before the tax department launches a full fraud case. File Form GST DRC‑03, pay the tax and interest upfront, and the penalty can be capped at 15 percent—far less than the 100 percent that applies once an order is passed.

India’s GST regime, rolled out in 2017 to replace a maze of indirect levies, still trips up many MSMEs through data mismatches, mis‑classifications, or simple clerical errors. When officials believe the lapse is deliberate—fraud, wilful misstatement, or suppression of facts—Section 74 springs into action. The language is tough, but the law also offers a practical escape route: settle quickly and avoid a Show Cause Notice (SCN) fight, court appearances, and reputational drag.

This guide explains the voluntary‑payment windows, the sliding penalty slabs, and the step‑by‑step process for filing DRC‑03 on the GST portal—so you can act before the meter starts running.

Understanding Voluntary Payment Under Section 74

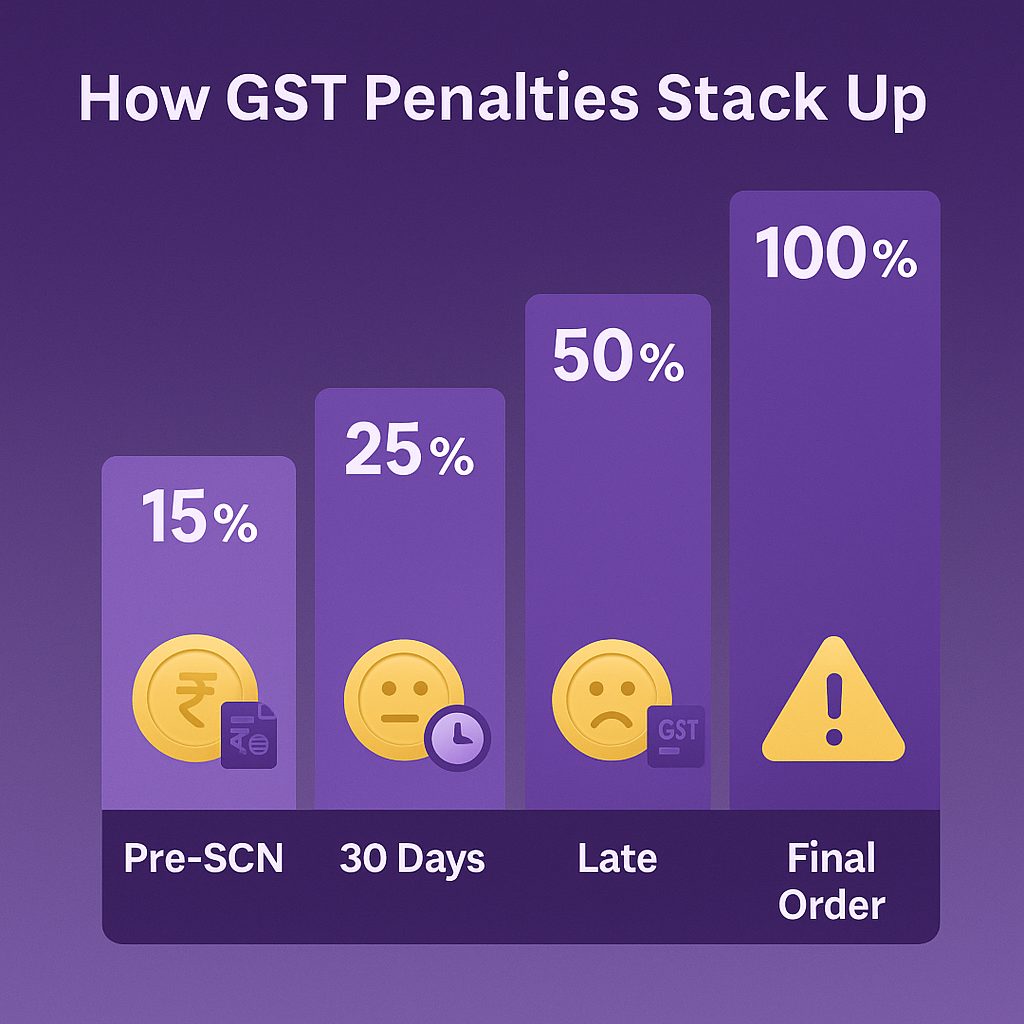

Voluntary payment under Section 74 lets a taxpayer clear the short‑paid tax, interest, and a reduced penalty by filing Form GST DRC‑03 either before a Show Cause Notice (SCN) is served or within 30 days of receiving one. Acting in this window can transform a potential fraud proceeding into a quick, paper‑driven closure.

Why it’s worth moving fast

- Penalty capped:

- Before an SCN – penalty is limited to 15 % of the tax amount.

- Within 30 days after an SCN – penalty rises to 25 %.

Missing both windows can push it to 50 % or even 100 % once an order is issued.

- Fewer legal headaches: Early compliance usually halts further summons, department visits, and reputation damage.

- Room for re‑classification: Where intent is debatable, many practitioners cite Rule 142(1A) letters to argue the case belongs under Section 73 (non‑fraud) with zero penalty—but only if the taxpayer engages swiftly.

Quick example

A wholesale trader discovers a ₹1 lakh GST short‑payment tied to mis‑classification. By filing DRC‑03 and paying tax plus interest before any SCN, the firm limits its penalty exposure to ₹15,000 and closes the matter—no prolonged correspondence, no courtroom stress. Delay beyond 30 days could have lifted that penalty to ₹25,000 or more.

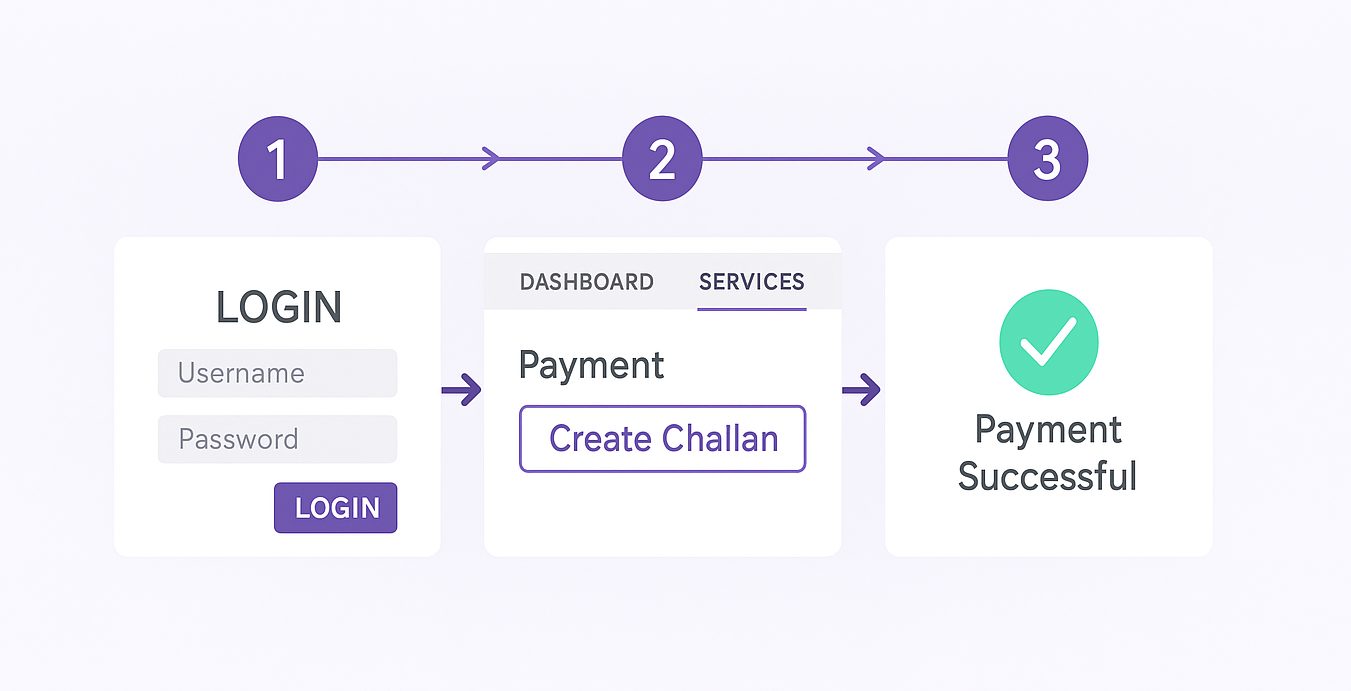

Procedure for Voluntary Payment Using Form GST DRC-03

To settle dues under Section 74, you must file Form GST DRC‑03 on the GST portal. The form works for both pre‑SCN and post‑SCN payments and records the tax, interest, and any applicable penalty.

Step‑by‑step on the portal

- Log in at www.gst.gov.in with your GSTIN credentials.

- Go to Services ▸ Payments ▸ Create Challan.

- Under Reason for Payment, choose Voluntary Payment (DRC‑03).

- Pick the relevant Act—CGST, SGST, IGST, or UTGST.

- Enter:

- Tax amount (short‑paid or unpaid)

- Interest (18 % per annum, auto‑calculated by the portal once you feed dates)

- Penalty — 15 % if you are paying before any Show Cause Notice, 25 % if within 30 days after an SCN.

- If you are responding to an SCN, quote the SCN reference number in the remarks box.

- Choose a payment mode (Net‑banking, NEFT/RTGS, credit card, or ledger adjustment where allowed) and complete the transaction.

- Download and save the DRC‑03 challan generated on success. Keep it with your working papers—the department may ask for it during reconciliation.

Pro‑tip: The portal keeps an un‑submitted DRC‑03 draft for 15 days—after that, it auto‑deletes. If you need internal approvals, export a PDF copy before the timer lapses.

You must file DRC‑03 before an SCN or within 30 days of receiving one to lock in the reduced‑penalty benefit.

For a visual walk‑through, the GSTN’s screenshot guide is handy:

https://tutorial.gst.gov.in/userguide/demandsandrecovery/Manual_GST_FORM_DRC-03.htm

Voluntary Payment Before SCN: Penalty Benefits

Paying up before the tax officer serves a Show Cause Notice is the cheapest off‑ramp you will ever get under Section 74.

| Timing of payment | What you settle | Penalty charged | Why it matters |

| Before SCN is issued | Tax + interest | 15 % of the tax | Lowest slab; no courtroom detours, no summons carousel. |

| Within 30 days after SCN | Tax + interest | 25 % of the tax | Still a bargain, but you’ve lost 10 points. |

| >30 days after SCN, before order | Tax + interest | 50 % of the tax | Penalty doubles; you’re in the long haul now. |

| After final order | Tax + interest | 100 % of the tax | Full freight, plus possible prosecution. |

Example:

A distributor uncovers a ₹1 lakh GST short‑payment tied to forged purchase invoices. If the firm pays before any SCN, the penalty caps at ₹15,000. Wait until the officer issues an SCN and those same dues will cost ₹25,000. Let it roll past 30 days and you risk a ₹50,000 hit—one‑half the tax amount—before interest even enters the picture.

Early payment also stops the notice from landing in public GST analytics dashboards, sparing you negative supplier or lender scrutiny.

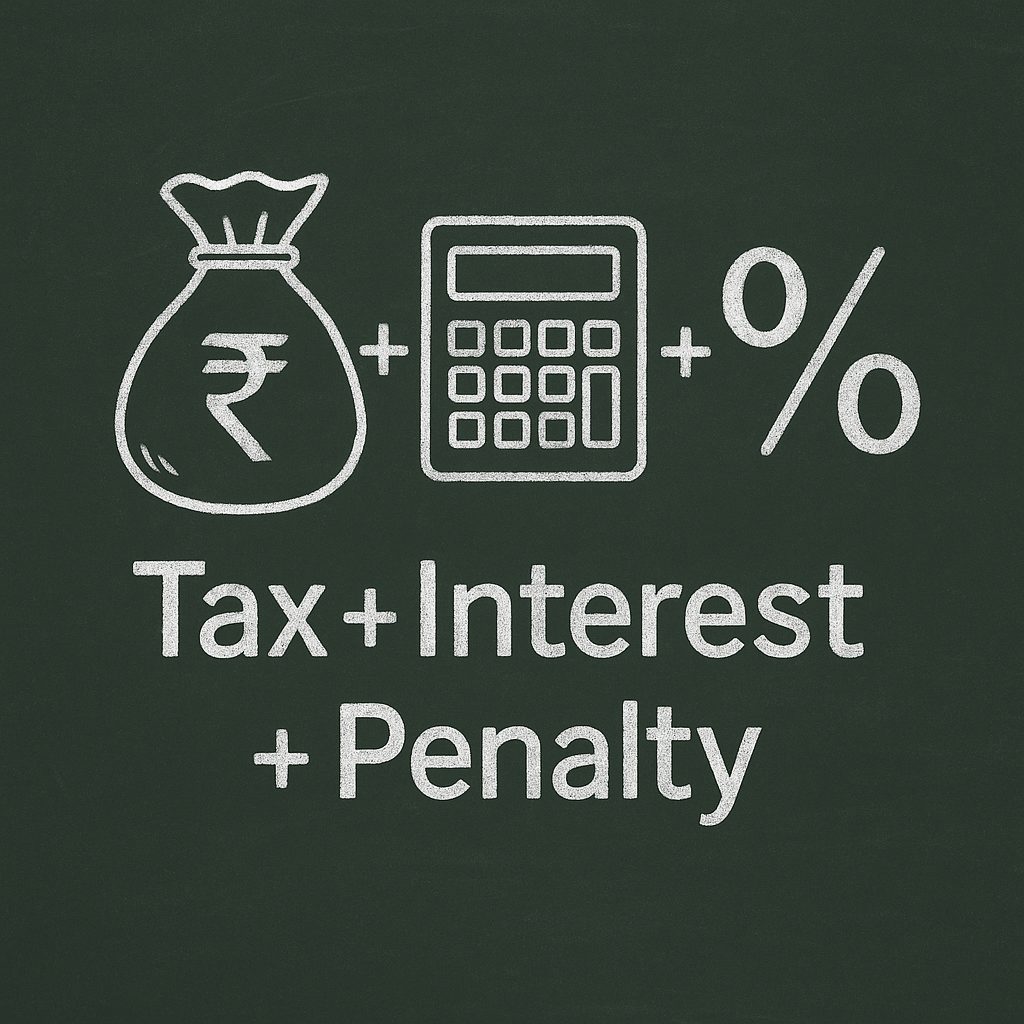

Tax Liability Under Section 74

When you opt for voluntary payment, you must clear three components—tax, interest, and the reduced penalty—in one go. The GST portal lumps these into a single DRC‑03 challan, but it helps to break the math down yourself first.

Formula

Total liability = Unpaid/short‑paid tax

+ interest (18 % p.a. under Sec 50(1), calculated per day from the original due date until you pay)

+ penalty (15 % if before SCN, 25 % if within 30 days after SCN)

Worked example

Suppose a trader failed to report taxable outward supplies worth ₹1 lakh for exactly one year:

| Component | Amount | How it’s derived |

| Short‑paid tax | ₹1,00,000 | Your undisclosed liability |

| Interest @18 % | ₹18,000 | ₹1,00,000 × 18 % × 1 year |

| Penalty (before SCN, 15 %) | ₹15,000 | ₹1,00,000 × 15 % |

| Total to pay | ₹1,33,000 | Sum of all three |

Delay the payment until after the SCN’s 30‑day window and the same penalty becomes ₹25,000, pushing total outflow to ₹1,43,000—proof that days really are money.

Heads‑up: Interest is simple, not compound, and it never vanishes—even if you convince the department to re‑classify the case under Section 73. Always double‑check the portal’s auto‑calculation against your own dates; manual overrides can be needed if you amended returns late.

Penalties and Interest Under Section 74

Section 74 uses a sliding‑scale penalty to nudge taxpayers toward early settlement. Memorise the slabs:

- 15 % of the tax – if you pay before any Show Cause Notice is issued.

- 25 % – if you settle within 30 days after receiving the SCN.

- 50 % – if you miss that 30‑day window but pay before the adjudicating order is passed.

- 100 % – if you pay after the order (the costliest lane).

Interest, always 18 % p.a., runs from the original tax due date to the day you pay—no discounts, no holidays, and it’s simple interest, not compound.

Quick illustration

A taxpayer evades ₹1,00,000 in GST:

| When liability is cleared | Penalty | Total cash outflow* |

| Pre‑SCN | ₹15,000 | ₹1,15,000 + interest |

| Within 30 days of SCN | ₹25,000 | ₹1,25,000 + interest |

| >30 days post‑SCN, pre‑order | ₹50,000 | ₹1,50,000 + interest |

| After order | ₹1,00,000 | ₹2,00,000 + interest |

*Interest (@18 %) is added to each scenario based on the delay, so the real cost creeps higher the longer you wait.

The maths alone tells the story: act fast, keep the cheque smaller, and shut the file before the penalties double or worse.

Show Cause Notice (SCN) Under Section 74

An SCN is the department’s formal way of saying, “We think you’ve under‑paid GST on purpose—prove us wrong or pay up.” The notice typically contains four elements:

- Alleged under‑payment – the amount and the tax heads (CGST/SGST/IGST).

- Grounds – why the officer believes fraud, wilful misstatement, or suppression of facts exists.

- Proposed penalty and interest – calculated as if you didn’t settle early.

- Response window – usually 30 calendar days from the date you receive the notice.

Your options once an SCN lands

| Path | What you do | Cost profile | Practical notes |

| Settle within 30 days | File DRC‑03, pay tax + interest + 25 % penalty | Second‑lowest slab | Department will issue an acknowledgement and drop the proceedings. |

| Contest | File a written reply, attach evidence, seek personal hearing | No payment now, but risk 50–100 % penalty later | Be ready with reconciliations, invoices, and intent proofs. |

| Do nothing | Ignore the notice | Worst‑case: 100 % penalty + attachment of bank a/c | Also risks cancellation of GST registration and prosecution. |

Tick‑tock: The 30‑day clock starts the day the notice is served—weekends count. Ask for an extension only if you genuinely need more time and can show effort (draft reply, partial data).

Tip for MSMEs

If the alleged fraud hinges on a clerical mismatch—say, an invoice number typo—attach GST‑matched ledgers, bank statements, and an affidavit explaining the mistake. Officers often re‑classify such cases under Section 73 (non‑fraud), wiping out the penalty entirely.

Consequences of Skipping Payment Under Section 74

Walk away from an SCN under Section 74 and the law stops playing nice:

- Penalty hits full throttle: the tax you owe is matched rupee‑for‑rupee—100 percent extra, no haggling.

- Interest keeps the meter spinning: 18 percent a year, calculated day‑by‑day until you square up.

- Bank accounts can go dark: officers may freeze balances or even lift inventory under Rule 159.

- Your GSTIN is at stake: lose it and customers won’t touch your invoices; vendors will cut ties too.

- E‑way bills? Denied. Trucks can’t move without them, so outgoing goods sit idle.

- Big amounts invite criminal heat: dodge more than ₹5 crore and you’re looking at a possible jail term—up to five years.

A story that stings

Last year a Jaipur‑based fabricator ignored a ₹10‑lakh SCN, assuming “it’ll sort itself out.” It didn’t. Six months later the adjudicating order doubled the bill. The tax office froze his company’s main current account the same week payroll was due. Vendors balked, projects stalled, and the business spent the next quarter fighting for working capital instead of chasing orders.

Lesson: pay early, sleep better.

Common Defences Against a Section 74 Show Cause Notice

A fraud‑tagged SCN doesn’t automatically make you guilty. Below are the arguments tax advisers reach for when the department’s case is shaky. Use the ones that fit your facts, and document everything—loose talk won’t cut it.

| Defence angle | When it sticks | What to show the officer |

| Fat‑finger errors | Numbers went wrong because someone keyed in “11,00,000” instead of “1,10,000,” or dropped a zero in HSN mapping. | Original invoices, amended returns, corrected ledgers—plus an affidavit explaining the slip‑up. |

| Grey‑zone interpretation | The Act or CBIC circulars are unclear, and you chose a reasonable reading—say, whether a SaaS export is IT or OIDAR. | Copies of circulars, advance rulings, industry position papers, and your internal tax memo documenting the choice made before the notice. |

| Time‑bar defence | SCN lands after the four‑years‑and‑six‑months limit (counted from the due date of your annual return). | Proof of filing date for GSTR‑9, SCN date stamp, and a simple timeline chart. |

| No evidence of intent | Department alleges suppression but can’t show emails, forged docs, or cash trail—just a mismatch. | Clean bank statements, e‑way bills that match books, and supplier confirmations; cite Rule 142(1A) and ask for Section 73 treatment. |

| Third‑party mismatch | The entire short‑payment arises from a vendor uploading the wrong GSTIN or invoice value. | Vendor’s written admission, revised GSTR‑1 snapshot, and correspondence showing you chased the correction. |

Real‑life save

A Pune SaaS start‑up got hit with a Section 74 SCN for classifying exports as zero‑rated services. They produced a 2022 advance‑ruling copy that backed their view, plus RBI FIRC receipts proving forex inflow. The officer re‑tagged the case under Section 73—penalty wiped, interest only till the filing date.

Pro tip: Always reply to the SCN within the 30‑day window, even if your defence is still cooking. A brief, factual letter reserving your right to add evidence buys goodwill—and sometimes an extension.

Section 73 vs Section 74 vs Section 74A — Spot‑the‑Difference Cheat Sheet

The GST Act gives officers three lanes for recovering unpaid tax. Pick the wrong one and the whole case can crumble on appeal, so it pays to know the markers.

| Feature | Section 73 (Non‑fraud) | Section 74 (Fraud / wilful misstatement) | Section 74A (New—Finance Act 2024) |

| Trigger | Slip‑ups, missed credits, plain arithmetic errors. | Intent to evade: false invoices, hidden sales, suppression of facts. | Minor / first‑time offences where tax at stake is ≤ ₹1 lakh and no repeat in 3 yrs. |

| SCN time‑limit | 2 yrs 9 mths from due date of annual return (GSTR‑9). | 4 yrs 6 mths from due date of annual return. | 4 yrs 6 mths (same as Sec 74). |

| Penalty if paid before SCN | 0 % | 15 % | 0 % (dept may waive penalty completely for small cases). |

| Penalty if paid ≤ 30 days after SCN | 10 % of tax (capped at ₹10 k) | 25 % of tax | 5 % of tax (draft rules—await final notification). |

| Penalty after adjudication order | 10 % (min ₹10 k) | 100 % | 30 % (proposed ceiling). |

| Interest | 18 % p.a. | 18 % p.a. | 18 % p.a. |

| Criminal prosecution | Rare. | Possible if tax evaded > ₹5 crore. | Not applicable. |

| Best for | Genuine clerical mistakes, ITC reversals, mismatched returns. | Fake invoices, cash sales off the books, forged e‑way bills. | Tiny errors by MSMEs—meant to unclog tribunals and give honest small players a chance to self‑cure. |

Heads‑up for 2025: Sections 74A draft rules still sit in the notification pipeline. Watch CBIC updates; once notified, voluntary payments under the ₹1‑lakh threshold could attract zero penalty if settled within 60 days.

Conclusion

Section 74 looks fierce on paper, yet it still hands you the steering wheel. Spot the under‑payment, run the maths, and clear the dues before the notice lands—or at worst, within that 30‑day grace period. Do that and the penalty’s a nick, not a hammer. Drag your feet and the slab jumps, interest piles up, bank accounts freeze, and the “fraud” tag lingers on credit checks.

Tata nexarc’s GST tools make the boring parts—error spotting, DRC‑03 calculation, portal screenshots—quick enough to tackle before lunch. And if you’re stuck between “pay” and “fight,” our compliance partners can read your data, flag soft spots, and draft the first reply so that 30‑day timer doesn’t own you.

Bottom line? Act while the line‑item is small, and the law stays on your side.

Empowering MSMEs to grow smarter

Tata nexarc delivers powerful solutions for MSMEs—discover tenders, access business loans, grow your online presence, and streamline procurement. Everything your business needs, all in one place.

FAQs

Can I revise or withdraw a DRC-03 after submitting it?

Is voluntary payment under Section 74 allowed if a GST audit or investigation has already started?

What documents should I keep after making a DRC-03 payment?

Can DRC-03 payments be made using balance in my electronic cash or credit ledger?

What if I paid under Section 73 instead of Section 74 by mistake?

Does making a voluntary payment under Section 74 affect my GST compliance rating?

Can I claim penalty or interest paid under Section 74 as a business expense for income tax?

How do I check if my DRC-03 payment has been accepted by the department?

Can I file a DRC-03 for each GSTIN separately if my business has multiple registrations?

What if I overpaid tax, interest, or penalty under Section 74—can I get a refund?

A product manager with a writer's heart, Anirban leverages his 6 years of experience to empower MSMEs in the business and technology sectors. His time at Tata nexarc honed his skills in crafting informative content tailored to MSME needs. Whether wielding words for business or developing innovative products for both Tata Nexarc and MSMEs, his passion for clear communication and a deep understanding of their challenges shine through.

every section has some sub section and its sub-section are so confusing. Always have to consult accountant for the same.

You can go through the link given on the article which has screenshot based guidance on the same. That will not create more confusion to you.