Table of Contents

Reverse Charge Mechanism (RCM) under GST is one of those rules that doesn’t make noise until it causes a problem. Many businesses follow it loosely or rely on accountants to flag when it applies, but with every GST Council meeting, the list of goods and services under RCM changes. The updates introduced in 2025 may look minor at first, but they carry real implications for businesses dealing with services such as transport, sponsorship, manpower supply, and legal consultancy. If you haven’t reviewed your RCM obligations recently, now’s a good time.

RCM rules have shifted again. Time to take a second look.

If you’ve been handling GST for your business, you already know what reverse charge is. It’s that one section most businesses tend to overlook until a mismatch shows up in GSTR-2B or a notice arrives.

As of April 2025, the GST Council has rolled out a few changes. Sponsorship services are no longer under reverse charge. There’s also a clarification on how input service distributors should handle inter-state RCM. It’s not a long list of changes, but the impact can be big, especially if you rely on third-party services or deal with transport, manpower, or legal consultants.

We’ve broken down the updated list of goods and services under reverse charge, along with the latest compliance requirements. Whether you’re new to GST or just reviewing your books before filing, it’s worth checking where you stand.

What is RCM?

Under GST, the normal process is that the seller charges tax on the invoice and pays it to the government. But reverse charge is when that responsibility shifts to the buyer. So instead of the seller adding GST, the buyer pays it directly.

This happens in some specific cases. One is when you’re buying from an unregistered supplier. The other is when the government has said that a certain good or service is covered under reverse charge. A few examples would be legal services, goods transport, or manpower supply.

If reverse charge applies, you’re supposed to raise a self-invoice and pay the GST yourself. Then you can claim input tax credit, but only if it’s done properly. If not, the credit might get rejected or flagged.

The rule isn’t new, but the list of items keeps changing. In 2025, a few adjustments have been made. Some services are back under forward charge. Others still need reverse charge treatment. That’s why it’s worth checking which ones apply to your business, so you don’t miss something or make a filing mistake.

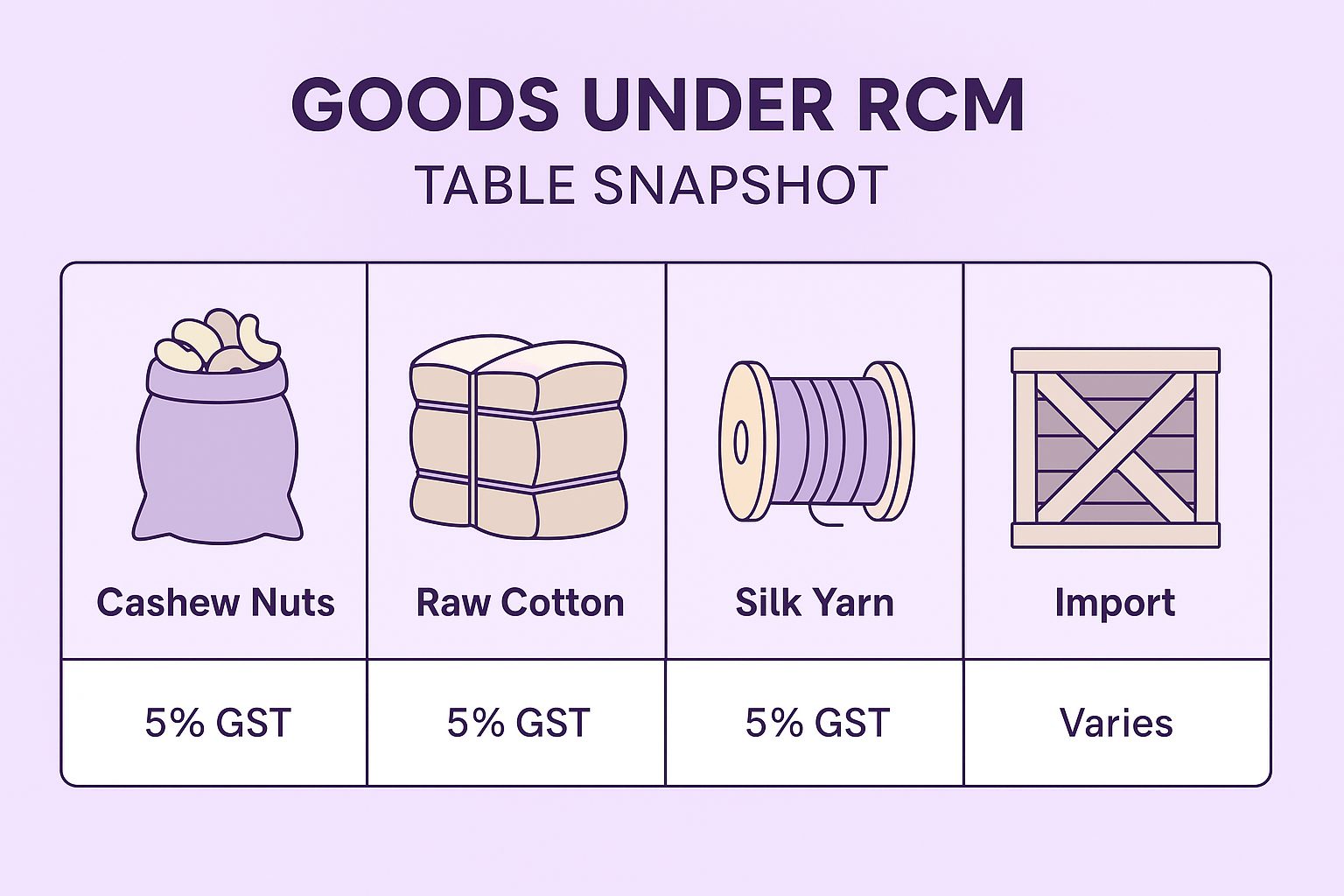

List of Goods Under Reverse Charge

There aren’t too many goods that come under reverse charge, but the few that are on the list come up a lot in day-to-day business, especially in industries like agriculture, forest produce, and textiles. Sometimes, GST isn’t charged by the supplier at all. Instead, the buyer ends up paying it straight to the government. That usually happens when the seller doesn’t have a GST registration, though in some cases it applies even if they are registered; depends on the type of goods or service.

Here’s a list of goods where reverse charge applies in 2025. Most of these are already known from past years, but it’s good to go over them again, especially with the government being stricter about documentation.

| Item | Seller Type | Buyer (Who Pays GST) | GST Rate | Remarks |

| Raw cashew nuts (unpeeled) | Agriculturist | Registered buyer | 5% | Only if the supplier is not registered. Common in food processing. |

| Bidi leaves | Forest gatherer or commission agent | Registered business | Possibly 40% or higher | Usually used in bidi manufacturing. Often bought informally. |

| Tendu leaves | Unregistered forest contractor | Registered buyer | 5% | Similar to bidi leaves, often seasonal. |

| Silk yarn | Unregistered dealer | Registered textile unit | 5% | Only reverse charge if the seller is unregistered. |

| Raw cotton | Agriculturist | Registered buyer | 5% | Comes up often in textile/fabric businesses. |

| Second-hand goods or used vehicles | Unregistered person | Registered reseller/dealer | Depends on margin | Applies if the dealer follows margin scheme. |

| Import of goods | Foreign exporter | Indian importer | As per IGST/customs | Always under reverse charge through customs. |

Note for 2025

The GST Council hasn’t added new goods this year, but they’ve made it clear that documentation has to be cleaner. If you’re buying from someone who’s not registered, even if it’s a regular vendor, make sure self-invoices are raised and GST is paid in time. A few cases have already come up where ITC was denied just because of missing invoices or delayed reporting.

This list is mostly based on the older notification with the relevant updates till now. No new items added in 2025 so far, but things do shift. So, check back around the next GST Council meeting.

Services Under Reverse Charge (2025)

More services fall under reverse charge than goods, and this list keeps shifting. If your business works with transporters, advocates, directors, or security staff through outside agencies, RCM is something you can’t ignore. These are the kinds of transactions where the seller doesn’t add GST; you have to take that up yourself.

A lot of businesses miss these or apply them inconsistently, which can cause ITC mismatches or show up as gaps during scrutiny. It’s best to go over this list once a year — and 2025 has brought a few important updates, especially in sponsorship and ISD-related services.

List of Key Services Under RCM

The following services fall under the Reverse Charge Mechanism (RCM) in 2025, meaning the recipient pays GST instead of the supplier.

| Service | Supplier | Recipient (Who Pays GST) | GST Rate | Remarks |

| Goods Transport Agency (GTA) | GTA (charging 5% without ITC) | Factory, Co-op, Firm, Company, Registered Person | 5% | RCM not applicable if GTA opts for 12% with ITC. |

| Legal Services | Advocate/ Law firm | Business entity | 18% | Covers advisory, consultancy & representation. |

| Arbitral Tribunal | Arbitral tribunal | Business entity | 18% | RCM applies to arbitration services. |

| Sponsorship Services | Any person | Company/Partnership firm | 18% | Recipient pays under RCM. |

| Govt. or Local Authority Services | Govt./ Local authority | Business entity | Varies | Applies to renting, FSI, or development rights. |

| Company Director Services | Director | Company | 18% | Company liable under RCM. |

| Insurance Agent Services | Insurance agent | Insurance company | 18% | Applies to commission or agent fees. |

| Recovery Agent Services | Recovery agent | Bank/NBFC | 18% | Applies to loan recovery and collection services. |

| Copyright/IP Services | Author/Artist/Composer | Publisher/Producer | 12–18% | RCM applies if creator hasn’t opted for forward charge. |

| Business Facilitator Services | Business facilitator | Bank | 18% | Common in rural banking setups. |

| Business Correspondent Agent Services | BC agent | Business correspondent | 18% | Applies to services under BC model. |

| Security Services | Non-body corporate (individual/firm) | Registered person | 18% | Not applicable for Composition or Govt. TDS cases. |

| Renting of Motor Vehicles | Non-body corporate | Body corporate | 5% | Applies if supplier opts for 5% without ITC. |

| Lending of Securities | Lender (via SEBI intermediary) | Borrower | 18% | Covered under SEBI’s Securities Lending Scheme. |

| E-commerce Platform Services | Individual via e-commerce | E-commerce operator | 18% | Includes cabs, accommodation, and housekeeping. |

| Import of Services | Foreign supplier | Indian recipient | IGST (as per rate) | Always under RCM for services from abroad. |

Changes to Watch in 2025

The big one this year is sponsorship services. They’ve moved out of reverse charge and are now taxed under forward charge. So, if you’re paying for event sponsorships or brand tie-ups, make sure the vendor issues a GST invoice. Also, there’s a new clarification on how inter-state service credit should be distributed by ISDs. If your head office pays for a service used by branches, double-check how you’re billing that — it may still need RCM treatment depending on the setup.

These rules haven’t changed much, but the way they’re applied is getting stricter. Some businesses got notices last year just for not raising self-invoices or misreporting services like director payments. It’s worth getting this list right.

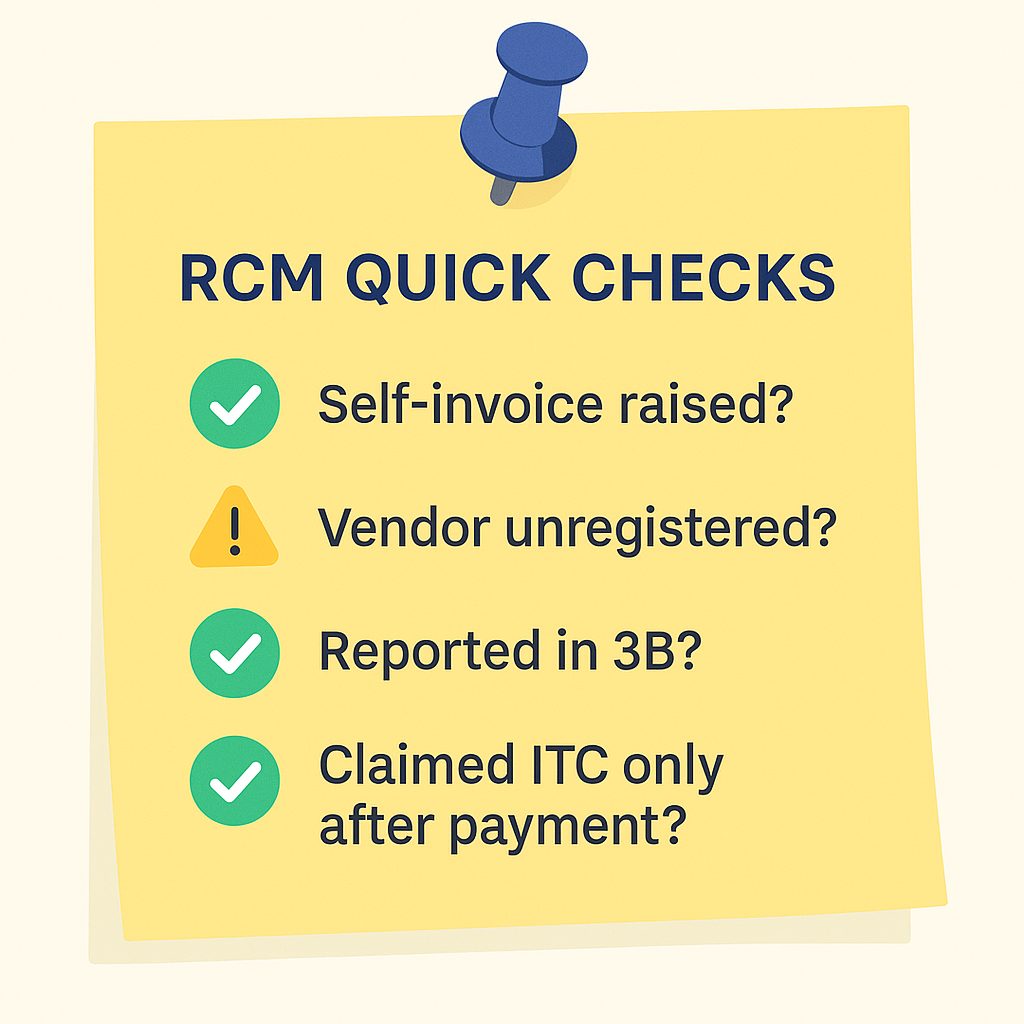

RCM Checklist for Day-to-Day Use

Reverse charge isn’t complicated, but it’s easy to miss steps if you’re not looking out for them. The law hasn’t changed much, but GST officers still catch people on basics such as not raising a self-invoice or claiming credit too early. Here’s a rough checklist. Doesn’t cover every case, but it’ll catch most of the common ones.

Before booking anything:

- Check if RCM applies to the item or service. Don’t go by memory, check the actual list.

- See if the supplier is unregistered. That’s usually when RCM applies.

- If it does, you need to raise a self-invoice. Still mandatory.

- Put a note on the entry – mark it clearly as reverse charge.

When you’re filing:

- Report the tax in GSTR-3B under the reverse charge section.

- Claim ITC only after the tax is actually paid. Not before.

- Use your self-invoice number, not the vendor’s bill number.

Every month:

- Go through payments made to freelancers, small suppliers, or any unregistered vendors.

- Keep a copy of each self-invoice somewhere, even if it’s a PDF folder.

- Before you file returns, cross-check your list. Most mistakes happen here.

RCM-Related Changes from the 56th GST Council Meeting

Not a huge list of changes this time, but there are a few updates businesses should take seriously. These won’t affect everyone, but if you’re handling services like sponsorship or dealing with cross-branch input credits, this matters.

Sponsorship services partially moved out of reverse charge

Until now, if a company paid for sponsorship, they had to handle GST under RCM. That’s changed but only for body corporates. From 16 January 2025, when a body corporate provides sponsorship services to another body corporate or partnership firm, the tax must now be paid under forward charge by the service provider. In other cases, RCM may still apply. So if your company sponsors events or influencer campaigns, make sure the vendor is billing GST correctly.

ISD (Input Service Distributor) compliance under focus

The Council reiterated that when a head office pays for services used across branches in multiple states, the credit must be distributed through the ISD mechanism — not booked under RCM. The GST department has been flagging non-compliance here, so businesses should align their internal accounting and registrations accordingly.

Self-invoicing Reminder

Still mandatory when purchasing from unregistered vendors under RCM, and now must be done within 30 days of receiving goods or services, as per Rule 47A. No relaxations or exemptions were introduced.

That’s about it for RCM from the 56th meeting. No sweeping new inclusions, but these clarifications, especially around sponsorship and ISD, can have significant compliance implications if ignored.

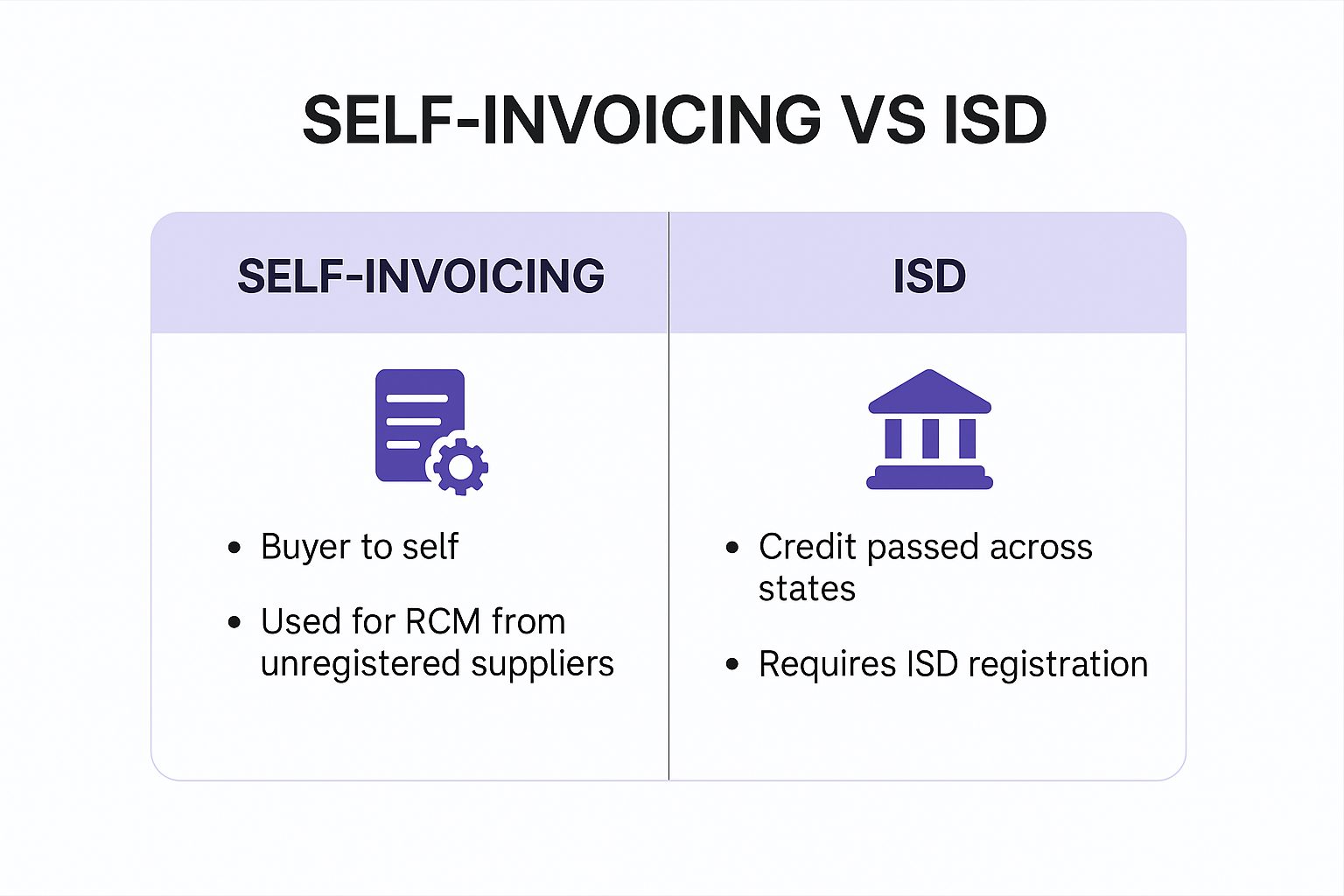

Self-Invoicing and ISD

If you’re buying from someone who isn’t registered under GST, and reverse charge applies, you have to make the invoice yourself. That rule hasn’t changed. A lot of people still miss this. You can’t just keep the vendor’s bill and file your return — GST law says you have to raise a proper invoice and pay the tax from your side.

It doesn’t have to be fancy. Just like a regular invoice — name, GSTIN, value, tax amounts, but mark it as “reverse charge.” Some use a fixed format for this. Others just use their standard invoice template and tweak it. Either works, as long as the details are right and it’s recorded on time.

On ISD — this is about how you pass on input tax credit between different GST registrations. If your head office pays for a service used by branches in other states, you can’t just rebook it through RCM or journal entries. You need an ISD registration and have to distribute credit through that. That’s the rule. The Council made that clear again this year. Some businesses were doing workarounds, but that’s not allowed anymore.

It’s not complicated, but it’s easy to overlook. Just raise the invoice. Register ISD if you need to. Don’t delay or skip it — GST officers are checking this more closely now.

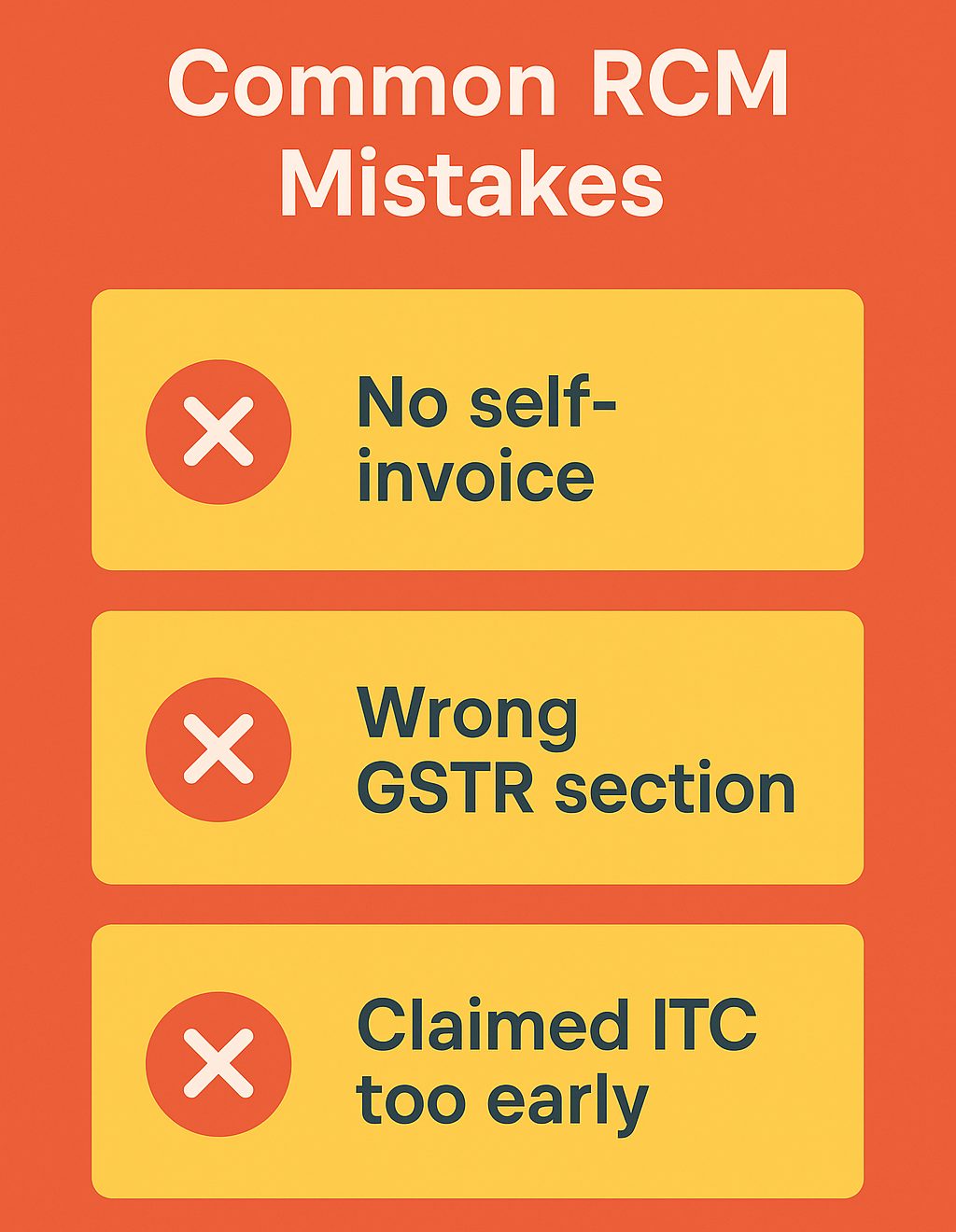

Common Mistakes

RCM looks simple on paper, but it’s one of the first things GST officers check during audits. Not because it’s hard — just because people miss the basics. And once there’s a pattern of mistakes, penalties stack up fast.

Here are some common slip-ups:

- Not raising a self-invoice

This is still mandatory. Doesn’t matter if the vendor gave you a bill. If they’re unregistered and RCM applies, you have to generate one. - Paying the tax, but not booking it properly

Some businesses pay RCM, but it doesn’t show up in the return the right way. Wrong section, or wrong reference number. That alone can block your credit. - Claiming ITC before paying the RCM amount

You can’t do that. You get credit after the tax is paid — not when you book the expense. - Missing RCM on services like director fees or legal help

These are easy to forget because they don’t come up every day. But they still count. - Trying to pass ISD transactions through journal entries or internal bills

Doesn’t hold up. If it’s a cross-state service and credit has to move, it must go through ISD. That’s the rule.

Penalties start with interest on short-paid tax, but they don’t stop there. If the officer sees consistent non-compliance, you’re looking at formal notices, credit reversals, and more paperwork than you want.

Key RCM Entries: 2024 vs. Oct 2025

| Entry/clause | Position in 2024 | Change by 2025 (what changed) | Effective date | Practical impact & taxpayer action |

| Sponsorship services (to body corporate/ partnership firm) | In many cases sponsorship services could be captured under RCM (recipient liable) as per earlier RCM notifications/interpretations. | Notification No. 07/2025 amended the RCM entries – RCM not applicable where a body corporate supplies sponsorship services to another body corporate or partnership firm; such suppliers will charge GST under forward charge. | Notification dated 16-Jan-2025, effective w.e.f. that notification date. | If you were paying GST under RCM for sponsorship to corporates, stop self-charging and obtain a normal tax invoice from the sponsor (forward charge). Update your accounting and GSTR reporting. Verify counterparties are body corporates/partnerships before changing treatment. |

| Renting of commercial/ immovable property by unregistered person → recipient under RCM | Not under RCM for unregistered landlords historically (till Oct 2024). | Notification No. 09/2024 inserted renting of immovable property (other than residential) by an unregistered person to a registered person into RCM list — making the tenant/recipient liable to pay GST under RCM. Later Notification 07/2025 clarified an exclusion — composition taxpayers as recipients are excluded from this RCM entry. | Initially effective 10-Oct-2024 (Notification 09/2024). Corrigenda/ subsequent amendments and exclusion for composition taxpayers via 16-Jan-2025 notification. | Registered recipients renting from unregistered landlords must self-invoice and pay GST under RCM — except if the recipient is a composition taxpayer (then excluded after 07/2025). Action: classify tenant status (composition or regular), update rent contracts, ensure self-invoicing & GSTR reporting for rent-RCM where applicable. |

| Time-of-supply/ self-invoice requirement for RCM on services from unregistered suppliers | Time-of-supply rules had been clarified by Finance Act changes in 2024; self-invoicing rules were being tightened. | Amendment in Section 13 (Finance Act 2024): strengthened time-of-supply rules where recipient must create self-invoice to pay under RCM for services from unregistered suppliers — failure to properly self-invoice/record can impact ITC eligibility. (This rule began applying from Nov-2024 onward.) | Effective 1-Nov-2024 (time-of-supply amendments). By 2025 the practice and enforcement expectations are firm. | Recipients paying under RCM must issue self-invoices when buying services from unregistered suppliers (and keep documentary proof). Ensure accounting systems create self-invoices, report RCM in GSTR-3B appropriately and claim ITC only after tax is paid. |

| ISD/ GSTR/ rule clarifications affecting RCM reporting & ITC distribution | Earlier rules on ISD, ITC distribution and GSTR form fields applied; formats evolving. | Notification No. 09/2025 (11-Feb-2025) and related CBIC notifications clarified effective dates and made changes to GSTR-7 / GSTR-8 / ITC distribution rules (and clarified aspects of handling RCM supplies in reporting, and ISD functioning). | Phased: several rule changes effective 11-Feb-2025 and some GSTR changes effective 1-Apr-2025 (as per notification timelines). | Review GSTR format changes (GSTR-7, -8, GSTR-3B invoice tables) and ISD procedures — ensure invoice-wise RCM reporting where required and that ITC distribution from RCM supplies is properly handled. Update ERP/GST reconciliation. |

| GST slab/ rate rationalisation (knock-on effect on RCM amounts) | GST had four primary slabs (5%, 12%, 18%, 28%) and certain items attract cess. RCM amount matched the applicable slab for the supply. | GST 2.0 / Fitment changes (56th GST Council) simplified slabs to 5% and 18% for most items, with a special 40% for select “sin/luxury” items — effective 22-Sep-2025 for most changes. RCM uses the applicable GST slab for that supply; therefore, the tax paid by the recipient under RCM changes where the underlying supply’s rate changed. | Decisions & fitment announced in Sept-2025; many rate changes effective 22-Sep-2025 (check item-wise fitment lists). | If you pay tax under RCM, update the rate applied on self-invoices/ liability entries according to the new fitment from 22-Sep-2025. Reconcile ITC pools where rates changed (some credits may relate to earlier, higher rates). See PIB/ GST Council fitment charts for item-level rates. |

Practical Checklist

- Inventory RCM transactions (rent, sponsorship, arbitral services, G.T.A. supplies etc.) for FY 2024-25 and FY 2025-26 and tag whether counterparty is: (a) body corporate, (b) unregistered person, or (c) you are composition taxpayer. (rent & sponsorship treatments changed).

- Update accounting rules so your system issues self-invoices automatically for RCM transactions (services from unregistered suppliers and rent from unregistered landlords) and uses the post-Sept-2025 GST slab where applicable.

- Revise vendor contracts (rental, sponsorship). Ensure GST invoicing terms match the current tax treatment (forward charge vs RCM). Ask sponsors who are body corporates to issue forward-charge invoices.

- GSTR/ ISD changes: review new GSTR formats (GSTR-7/-8/-3B) and ISD distribution rules from CBIC notifications (Feb/Apr 2025 dates) and ensure your filings reflect invoice-wise RCM reporting where required.

- Train tax team / auditors — RCM misreporting can deny ITC or attract interest and penalties. Keep the notification PDFs / fitment lists for audit trails.

Who Should Pay Attention to RCM in 2025?

In 2025, the Reverse Charge Mechanism (RCM) continues to be a crucial area for businesses of all sizes, especially those that regularly deal with suppliers or service providers outside the GST network. Micro, small, and medium enterprises (MSMEs) should pay close attention, as many still buy goods or services from local or unregistered vendors. In such cases, the buyer — not the seller — is responsible for paying the GST under RCM. This often happens in sectors like manufacturing, textiles, and construction, where small suppliers may not be registered.

MSMEs Buying from Unregistered Vendors

Many MSMEs source raw materials or services from small, local suppliers who are not registered under GST. In these cases, the buyer must pay GST directly under RCM. This applies commonly in sectors like textiles, food processing, and construction. Failing to pay RCM on such purchases can lead to ITC rejection or penalties. Keeping records and self-invoices updated is key for smooth compliance.

E-commerce Sellers Using Third-Party Logistics

Online sellers often depend on third-party logistics and courier partners for order fulfilment. If the transporter or service provider is unregistered, RCM liability can shift to the e-commerce seller. Charges for shipping, warehousing, or handling may attract RCM based on registration status. Regular checks of vendor GSTINs help prevent reporting errors. This ensures sellers stay compliant and avoid credit mismatches.

Professional and Consultancy Service Users

Businesses that use services like legal advice, manpower supply, or technical consultancy often fall under RCM. For these, the service provider may not charge GST — the client must pay it directly. The GST rate usually applies at 18%, with input credit available after payment. Many companies miss these payments because they happen infrequently. Having a monthly RCM review helps ensure all such services are captured.

Importers of Goods and Services

Any business importing goods or services from outside India automatically falls under RCM. In such cases, the importer pays IGST on the transaction, even if the supplier is overseas. The payment is usually made during customs clearance or in the GST return. This rule applies to both tangible goods and digital or consulting services. Properly reporting imports ensures input tax credit can be claimed later.

Companies Paying Directors or Government Fees

When a company pays sitting fees, commissions, or consultancy charges to directors, RCM applies. The company must pay GST directly instead of the director charging it. Similarly, certain government services (like renting or licensing) also fall under RCM. These payments are often small but closely monitored during audits. Maintaining clear documentation and timely payment keeps compliance hassle-free.

Conclusion

Reverse charge under GST isn’t complicated, but it’s strict. You either follow the steps or you don’t — there’s not much room in between. The list of goods and services changes a little each year, but the process stays the same: check the rules, raise the invoice, pay the tax, and claim the credit only when it’s due.

If you’re handling this in-house, build it into your monthly routine. And if you’re not sure whether a transaction falls under RCM, don’t guess — check, or ask.

Missing a few entries here and there might not seem like a big deal, but over time, they add up. Better to catch them early than explain them later.

Empowering MSMEs to grow smarter

Tata nexarc delivers powerful solutions for MSMEs—discover tenders, logistics solutions, and streamline procurement. Everything your business needs, all in one place.

FAQs

Does RCM apply to intra-state or inter-state transactions?

RCM can apply to both, depending on the nature of the supply and the supplier’s registration status.

Can freelancers or consultants charge GST under RCM?

Is RCM applicable on import of services from foreign companies?

Can RCM be applied voluntarily if both parties agree?

No. RCM applies only to notified categories. You can’t opt-in voluntarily if the transaction doesn’t fall under RCM by law.

Is GST under RCM applicable on advances paid to unregistered vendors?

Can RCM liability be adjusted against input tax credit (ITC)?

Do I need to issue an e-invoice for self-invoicing under RCM?

No, e-invoicing is not required for self-invoicing under RCM, even if you cross the e-invoice threshold.

Is TDS or TCS applicable on RCM-based payments?

Are transport services always under RCM?

How long should I keep self-invoices and RCM records?

A product manager with a writer's heart, Anirban leverages his 6 years of experience to empower MSMEs in the business and technology sectors. His time at Tata nexarc honed his skills in crafting informative content tailored to MSME needs. Whether wielding words for business or developing innovative products for both Tata Nexarc and MSMEs, his passion for clear communication and a deep understanding of their challenges shine through.

If I get fabric manufactured by an unregistered weaver on job work basis, Do I have to pay RCM on job work??