Table of Contents

- Introduction – Why Steel Decarbonisation Matters

- What Is Steel Decarbonisation?

- Global Momentum and Market Shifts

- India’s Steel Decarbonisation Landscape

- MSME Challenges in Low-Carbon Transition

- Opportunities for MSMEs and Buyers

- Financing and Risk Management

- Supply Chain and Workforce Readiness

- Case Study Snapshots from Clusters

- Conclusion – A Business Imperative for MSMEs

- FAQs

Introduction – Why steel decarbonisation matters globally and in India

Steel decarbonisation is no longer an abstract goal. It is starting to shape how business is done – from vendor registration to tender qualification. Across India, both government and private buyers are asking suppliers to show that their production methods are cleaner and more efficient.

For smaller steel producers, fabricators, and contractors, this marks a turning point. What used to be an environmental discussion has become a commercial requirement. Buyers now weigh carbon credentials alongside delivery time and pricing. In large infrastructure projects, sustainability checks are being added to bid documents and supplier scorecards.

Even global policies are driving change. Europe’s Carbon Border Adjustment Mechanism (CBAM) requires exporters to declare the carbon content of steel products. India’s own Carbon Credit Trading Scheme has created the framework for reporting and trading emission reductions. Together, these measures are pulling even smaller suppliers into formal carbon accounting systems.

For businesses, ignoring these changes is never an option. It can mean lost contracts or lower buyer preference. But compliance doesn’t have to be expensive. The first steps are practical: track energy use, keep records of raw material sourcing, and start aligning documentation with buyer formats. These basic measures signal readiness – and in the current market, readiness often decides who wins the order.

What is steel decarbonisation?

Steel decarbonisation means cutting down the carbon released during steelmaking and its use. The most common production route in India – the blast furnace to basic oxygen furnace (BF-BOF) system – depends heavily on coal and coke. This method is energy-intensive and emits nearly two tonnes of CO₂ for every tonne of crude steel produced.

Why steel is such a heavy emitter

Unlike many other industries, steel requires both extreme heat and a chemical reaction to separate oxygen from iron ore. Coal here acts not just as a fuel but also as a reducing agent, which makes substitution complex. This is why steel is labelled a “hard-to-abate” sector. For MSMEs in re-rolling, fabrication, or secondary supply, the emissions problem extends further. Power consumption, transportation, and even the source of sponge iron or pellets all add to their footprint.

Pathways to reduce emissions

Decarbonisation in steel is not one single fix. It involves a set of evolving technologies and practices that are gaining traction worldwide:

- Electric arc furnaces (EAFs), when run on renewable electricity, cut out coal and reduce direct emissions.

- Hydrogen-based direct reduced iron (DRI) can replace coal in the reduction process, although it remains costly and infrastructure-heavy today.

- Scrap recycling and circularity reduce the demand for fresh ore and keep emissions in check.

- Carbon capture, utilisation and storage (CCUS) helps capture gases at source and either store or repurpose them.

- Alternative inputs like biomass, green iron, or specially processed pellets are being piloted as supplementary options.

For smaller businesses, most of these routes are still aspirational. Yet understanding them is crucial, because larger buyers and policymakers are already embedding such methods into future standards. In practice, MSMEs will be expected to align their supply and compliance documentation with these pathways, even if they are not adopting them directly today.

Global momentum in steel decarbonisation

Across the world, steelmakers are moving from pilots to large-scale trials of low-carbon technologies. In Sweden, H2 Green Steel is now being produced with hydrogen instead of coal. Additionally, ArcelorMittal has begun blending hydrogen into its European furnaces and is testing carbon capture to trap emissions before release. Similarly, Japan and South Korea are also advancing capture-and-storage projects. On the contrary, China is aggressively scaling electric arc furnace (EAF) capacity. These examples show that the debate is no longer about feasibility but about the pace of adoption.

Buyers setting new benchmarks

The push is not limited to producers. Global buyers, especially in construction and automotive, are rewriting procurement rules to include environmental performance. The European Union’s Carbon Border Adjustment Mechanism (CBAM) already requires exporters to declare the carbon footprint of their steel. In parallel, green steel certification schemes are taking hold in Europe and North America, setting new expectations for suppliers worldwide.

This shift has also brought a language problem. Terms such as “steel decarbonisation” and “green steel” are often used as if they mean the same thing, but they do not. For businesses responding to tenders or preparing compliance documents, understanding the difference is more than semantics – it can decide whether a bid looks credible.

Steel Decarbonisation vs Green Steel

Here’s how the two terms compare in practice:

| Aspect | Steel Decarbonisation | Green Steel |

| Definition | Broad term for cutting emissions in steelmaking | Steel made with near-zero fossil fuel input |

| Scope | Includes efficiency upgrades, EAFs, hydrogen DRI, CCUS, and scrap recycling | Narrower, usually hydrogen DRI and EAF powered fully by renewables |

| Buyer perception | Seen as progress toward sustainability | Marketed as a premium, climate-friendly product |

| MSME relevance | Achievable in phases, tied to documentation and sourcing choices | Less accessible today due to limited supply and higher cost |

Why this matters to Indian MSMEs

For MSMEs supplying steel, fabrications, or re-rolled products, these shifts will arrive through contracts and buyer audits. Export-linked units may be asked for carbon intensity labels sooner than expected, while domestic tenders are beginning to adopt similar checks. MSMEs do not need to leap straight into green steel, but they must at least start aligning with decarbonisation pathways and prepare compliance records. The global momentum makes one thing clear: the pressure will flow down the supply chain, and those unprepared risk being locked out of future opportunities.

Steel Decarbonisation in India: The current landscape

India’s steel story is growing bigger every year. The country is already the world’s second-largest producer, and demand is only rising as highways, metro networks, industrial parks, and housing projects expand. This scale also makes the sector a major source of emissions, which is why steel has been placed at the centre of India’s climate strategy. What happens in this sector will decide how credible India’s 2070 net zero pledge looks to the world.

Also read: Steel Mahakumbh 2025, what it is and why MSMEs should care

Policy direction from the Centre

The Ministry of Steel has released a roadmap that pushes for three clear shifts: more scrap usage, a larger share of electric arc furnaces (EAFs), and a gradual move toward hydrogen-based direct reduced iron (DRI). Backing this is the National Green Hydrogen Mission, launched in 2023, which is financing pilot projects to test hydrogen use in steelmaking. These signals matter because they show where policy support and future incentives will concentrate.

Carbon Credit Trading Scheme (CCTS)

The Carbon Credit Trading Scheme, introduced in 2024, created a national framework for trading verified emission reductions. For now, it is large plants that are participating, but the design clearly anticipates the inclusion of smaller producers over time. For MSMEs, this points to an eventual need to measure and disclose emissions in recognised formats – not just for regulators but also for buyers who will demand such data as part of contract terms.

Incentives under discussion

As of September 2025, the government was weighing a ₹5,000 crore scheme to support cleaner steel technologies, prioritising hydrogen DRI and carbon capture. Some states, notably Odisha and Chhattisgarh, are also exploring renewable-linked subsidies for steel units. While the details on MSME eligibility are still vague, the direction of policy is unmistakable: those adopting cleaner technologies will be favoured in financing and procurement.

Why this matters for MSMEs

Even if the initial push targets large integrated producers, the ripple effects will reach smaller businesses quickly. MSMEs that supply fabricated components, re-rolled products, or inputs for infrastructure projects will be asked for emission data and sustainability declarations by bigger contractors. In public government tenders too, these requirements are expected to tighten. Firms that prepare early by collecting basic emission information and aligning with reporting formats will face fewer risks of rejection or contract loss.

MSME Challenges in transitioning to low-carbon steel

The shift to low-carbon steel is no longer optional. Yet, for most smaller businesses, the transition looks less like an opportunity and more like a series of roadblocks. MSMEs – whether they are re-rollers, small foundries, or fabrication units – are expected to adapt quickly, but the conditions around them are far from ready.

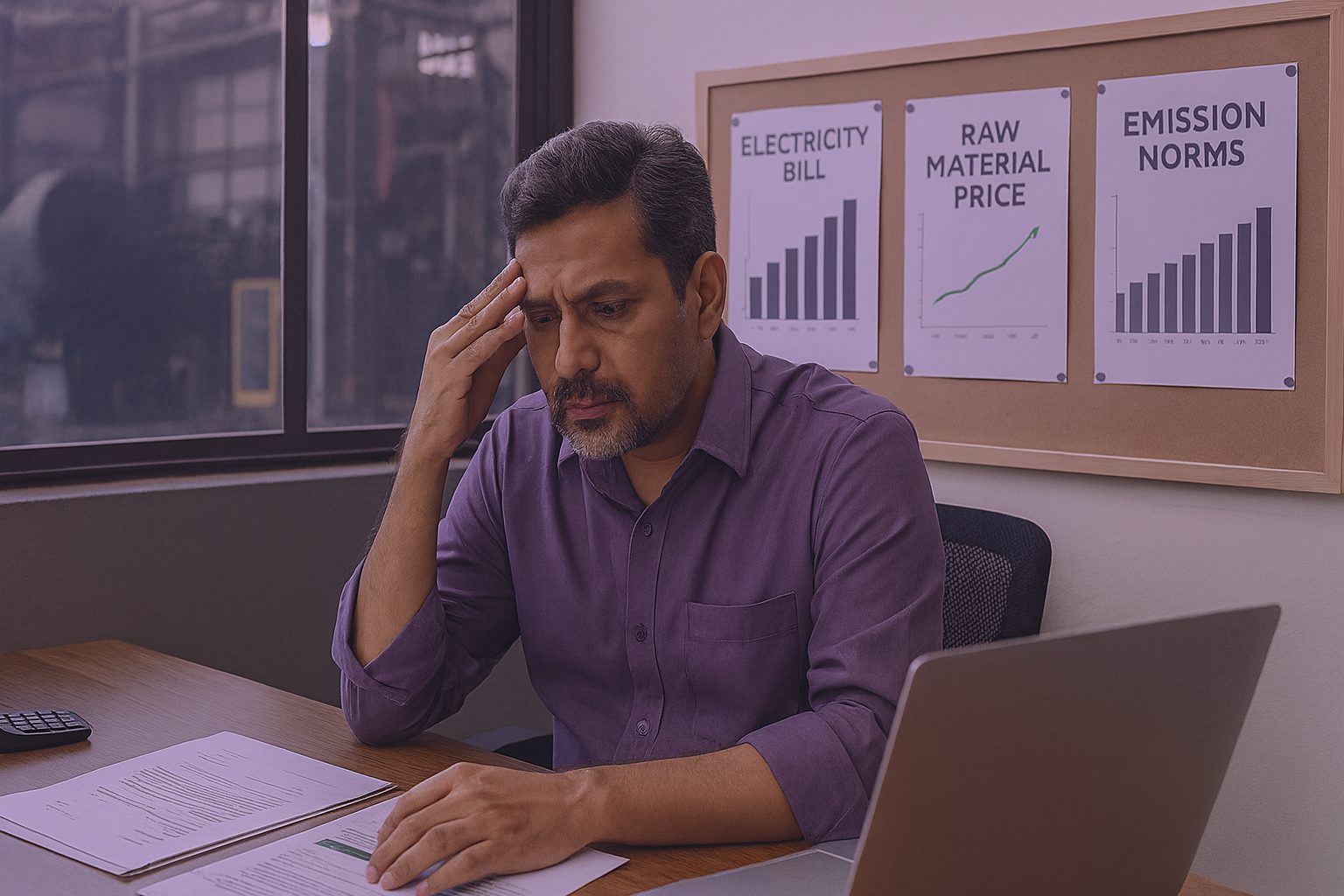

Capital constraints

Upgrading technology requires serious money. Installing electric arc furnaces or investing in hydrogen-ready equipment costs far more than what most MSMEs can raise. Even energy-efficient retrofits stretch budgets. Credit remains difficult, and there are still no mainstream financing products designed specifically for small steel producers. Without targeted financial support, the path to cleaner steel is economically out of reach.

Compliance pressures

Documentation has become a silent deal-breaker. Increasingly, tenders ask for emission reports or carbon footprint declarations. Large players can hire consultants and set up digital monitoring. Smaller firms cannot. As a result, bids are rejected not because the steel is poor or the price is uncompetitive, but because the paperwork does not meet the new standards.

Weak supply ecosystem

Even motivated MSMEs face shortages of clean inputs. Scrap is expensive and unevenly distributed, renewable electricity is costly at the retail level, and hydrogen supply is still at pilot scale. The ecosystem needed for small firms to transition simply does not exist today.

Risk of downtime

MSMEs cannot shut their operations for extended upgrades. For a small rolling mill or fabrication shop, a few weeks of downtime means lost orders and clients moving elsewhere. Any transition plan that does not account for business continuity is unlikely to succeed at the ground level.

Opportunities for MSMEs and buyers

While the push to decarbonise steel is often seen as a burden, it also opens doors for smaller businesses that act early. With global buyers, financiers, and government tenders moving toward sustainability criteria, MSMEs can use this moment to strengthen their position in supply chains.

Safeguarding export markets

European rules under the Carbon Border Adjustment Mechanism (CBAM) now require exporters to declare the carbon content of their steel. Indian MSMEs that provide clear emissions data – even if they are not yet producing fully green steel – can maintain their contracts and avoid being replaced by competitors who are better prepared. In global trade, reliable documentation can be the difference between keeping or losing a buyer.

Accessing new finance

Banks and investors are under pressure to back low-carbon industries. This is leading to ESG-linked loans and credit schemes tied to sustainability performance. MSMEs that start measuring and reporting emissions, however basic, will find themselves better placed to negotiate finance. Over time, lenders will treat environmental records as part of standard credit checks.

Gaining ground in procurement

Government projects and large private contracts are introducing sustainability clauses in tender conditions. A small unit that can provide a carbon footprint statement will have an advantage over one that cannot. Contractors managing strict audits also prefer MSME partners who reduce compliance risks in the supply chain.

Reducing future risks

Finally, there is a strategic benefit. Firms that build processes slowly will not have to face any sudden challenges as rules tighten. On the contrary, those who wait for risk disruption may put themselves in trouble, such as higher costs and lost orders when compliance becomes unavoidable.

Financing and risk management options

For small and medium steel units, every investment decision is tied to cash flow. The intent to modernise is there, but money – and the structure to support it – remains the missing piece.

Limited clarity on incentives

Policy signals are encouraging, but execution is still slow. The government has also outlined a ₹5,000-crore plan to promote low-carbon technologies such as hydrogen-based steelmaking and carbon capture. A few states, including Odisha and Chhattisgarh, are designing power subsidies for plants that shift to renewable energy. These initiatives point in the right direction, yet smaller units are waiting for clarity. Access conditions, application processes, and compliance requirements are still being worked out, and until then, most MSMEs can only prepare on paper.

Carbon credits – potential, but not immediate relief

The carbon trading system launched last year gives large producers a head start in earning and selling emission credits. In theory, this framework could help smaller firms too. In practice, most MSMEs do not yet have the systems to measure reductions accurately. For now, their best option is to align with larger buyers already participating in carbon markets – a step that keeps them visible in cleaner supply chains and helps them learn how the mechanism works.

Phased investment is the only realistic route

For most small steel producers, shutting operations for a complete technology change is impossible. Incremental improvement is the only workable strategy – using more scrap, replacing older furnaces with energy-efficient models, or adding monitoring systems that track fuel use. Some suppliers have begun offering lease or service models for new machinery, spreading out costs and reducing risk.

The value of planning early

When stricter emission rules arrive – and they will – financing will favour businesses that are already documenting their progress. Firms that start tracking energy consumption and estimating retrofit costs now will be in a stronger position to access credit or incentives later. Preparing early is less about compliance and more about keeping options open in a market that’s quickly changing its expectations.

Supply chain and workforce readiness

Technology and finance are only part of the decarbonisation story. The other two challenges – supply chain and workforce – are often overlooked but deeply connected. Without reliable access to cleaner inputs or a trained workforce, even the best technology plan stays on paper.

The supply gap

Most MSMEs rely on raw materials like sponge iron, billets, or scrap supplied through fragmented local networks. Access to good-quality scrap remains limited, and prices fluctuate sharply. Green hydrogen and renewable power, two key inputs for low-carbon production, are still expensive or unavailable in many industrial clusters. Large integrated producers may find ways to absorb these costs, but smaller units cannot. Until supply chains for cleaner inputs become stable, MSMEs will struggle to move beyond token sustainability measures.

Transport and logistics bottlenecks

Decarbonisation also depends on how efficiently materials move. Poor connectivity, delays in freight handling, and uneven access to rail networks keep logistics costs high. For many MSMEs, switching to low-emission transport options is not yet feasible because last-mile supply chains are fragmented. In effect, the cost of inefficiency in logistics cancels out much of the progress made in production efficiency.

The skills challenge

Low-carbon production requires new skills – from energy management to data tracking and equipment handling. Most MSMEs operate with small teams trained on conventional methods. Safety protocols for handling hydrogen, operating electric furnaces, or running emission monitoring systems are still new to the workforce. This skill gap can quickly become a compliance risk if not addressed through targeted training and industry-led skilling programmes.

Partnering for readiness

A few industry clusters have started pilot programmes where equipment suppliers, local industry associations, and technical institutes train workers on-site. Expanding such partnerships is critical. MSMEs cannot afford long downtime for classroom training, so skilling must happen within working hours and with clear, practical outcomes.

Case study snapshot: Grounded examples from clusters

Change rarely happens as dramatic overhauls in small units. In India, many MSMEs are already making small, data-driven adjustments under cluster programmes that reduce costs while edging toward cleaner operations.

Coimbatore foundry cluster: Baseline monitoring and motor right-sizing

In Coimbatore, a BEE-UNIDO programme encouraged foundry units to install energy monitors and revisit motor capacities. One documented intervention replaced a 7.5 kW motor, a 4 kW unit, and two 1.5 kW motors with better matched lower-power combinations. That single step reduced energy consumption noticeably, enabling participating units to improve their energy intensity.

Named foundry pilots: Adopting core process changes

Under the UNIDO-GEF-BEE scheme, several foundries adopted discrete technological changes for better efficiency. For example, Veesaa Foundry installed a modern compressed air system, and Bright Castings adjusted its core making processes. These are real units, cited in project documentation, showing that process-level tweaks are already in motion.

Eastern zone SRRM cluster: Technical support for 80 units

In the Eastern region (West Bengal, Jharkhand, Odisha, Bihar), UNIDO’s steel re-rolling sector compendium reports that 80 MSME units are being supported with technical upgrades and capacity building to adopt energy efficiency and renewable measures. These units now serve as local benchmarks in their clusters.

Conclusion: Why decarbonisation is a business imperative, not a choice

India’s steel industry stands at a turning point. The global shift toward low-carbon production is reshaping how contracts are awarded, how banks lend, and how buyers choose suppliers. For large producers, the message is already clear. For MSMEs, the change is catching up quickly – not as a regulation, but as a business requirement.

Across supply chains, emissions data is slowly becoming part of standard paperwork. Government tenders are testing sustainability criteria, and export buyers are asking for carbon footprints along with quality certificates. For small and medium enterprises, this means decarbonisation is no longer about future readiness – it is about staying in the market today.

The good news is that the first steps do not require massive spending. Tracking energy use, adopting efficiency measures, and maintaining transparent records can help MSMEs meet upcoming requirements. Over time, these practices will also improve margins and reduce dependence on volatile energy costs.

The industry’s direction is set. Those who act early will secure credibility and long-term buyers; those who wait will face shrinking options. In a sector built on competitiveness and reliability, sustainability has become the new measure of both.

FAQs

Will buyers pay more for green steel?

How can small suppliers align with a large buyer’s sustainability plan?

Will production costs rise with decarbonisation?

How will decarbonisation affect MSME participation in tenders?

How can MSMEs prepare for the EU’s Carbon Border Adjustment Mechanism (CBAM)?

Can shared service providers handle carbon accounting for MSMEs?

What training is available for MSME workers on low-carbon operations?

Why should non-exporting MSMEs still care about decarbonisation?

What role can industry clusters play in making decarbonisation affordable?

Are emission reporting tools affordable for small manufacturers?

Charul is a content marketing professional and seasoned content writer who loves writing on various topics with 3 years of experience. At Tata nexarc, it has been 2 years since she is helping business to understand jargon better and deeper to make strategical decisions. While not writing, she loves listing pop music.