Table of Contents

Ask any small exporter in Tirupur, Morbi, or Ludhiana what keeps them up at night, and the answer is rarely about finding orders. It’s about getting paid. A single delay in receiving money can throw everything off balance — wages, supplier dues, even rent.

This is where the letter of credit (LC) steps in. Think of it less as a fancy banking tool and more as a shield. Instead of relying only on the buyer’s promise, you rely on their bank. If you ship the goods and submit the right papers, the bank pays you. It’s that direct.

I’ve sat with MSME owners who thought LCs were only for exporters shipping containers to Europe or the US. The truth is, they’re just as useful if you’re sending a truckload of tiles from Morbi to Delhi or machine parts from Rajkot to Pune. For a small firm, an LC can be the thin line between a safe deal and a painful loss.

Of course, the first reaction is usually hesitation: “Isn’t this too complicated? Will my bank even bother with my small order?” Those doubts are real. But once you understand the meaning and types of LCs, the picture changes. You see that it’s not about size, it’s about security. And for a business that lives and dies on cash flow, that security matters more than anything else.

What is a Letter of Credit (LC)?

Think of a letter of credit as a safety switch. When you’re running a small unit — say, a tile factory in Morbi or a garments shop in Tirupur — you can’t afford to wait and wonder if the buyer will pay. An LC takes that fear out of the deal.

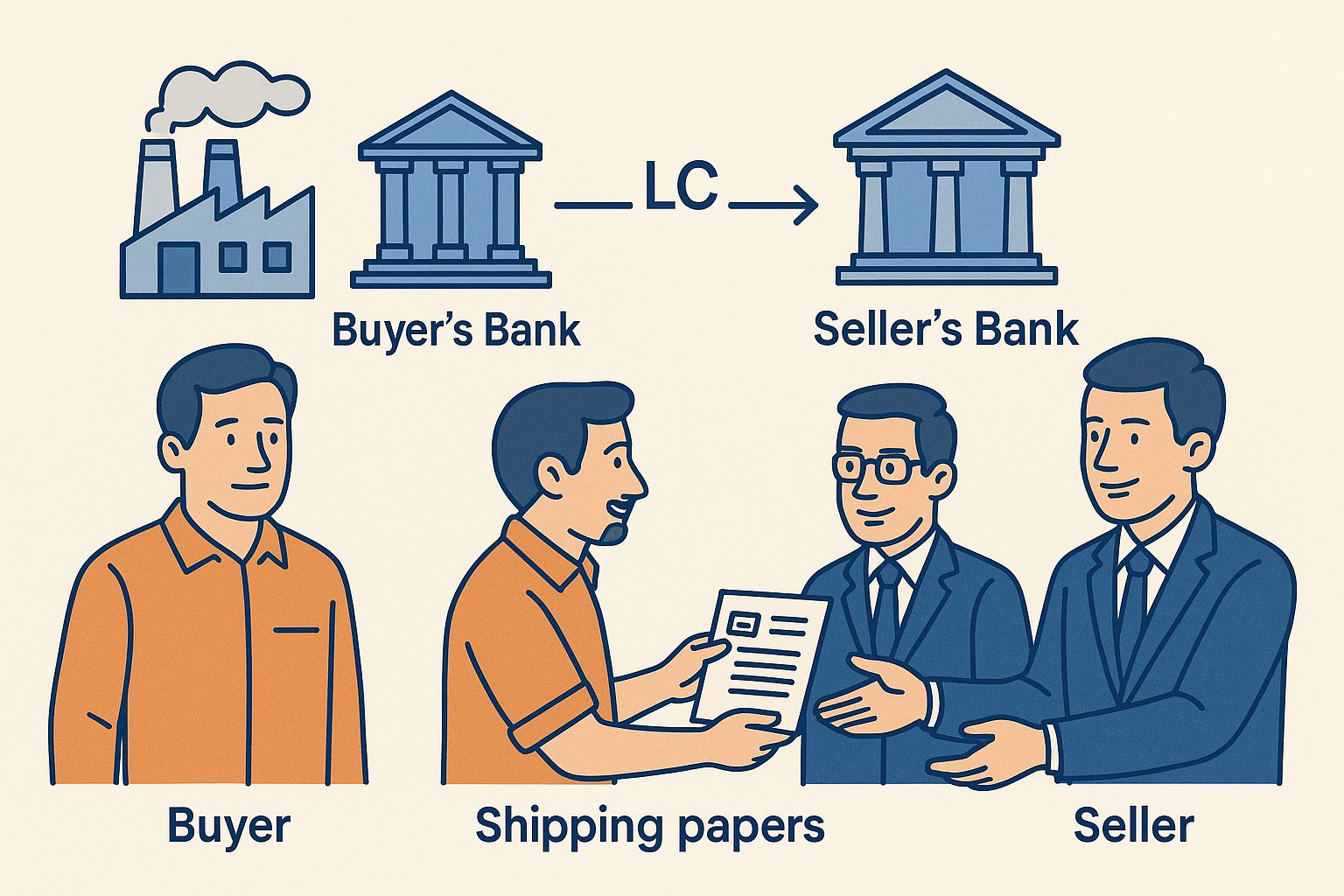

Here’s how it usually plays out. A buyer approaches you with an order. You don’t fully know them, maybe they’re based overseas or maybe they’re a big corporate in another state. Instead of shipping first and praying later, you ask them to route payment through their bank. That bank issues a letter of credit in your favour. Once you ship the goods and hand over the right set of documents — invoice, bill of lading, insurance papers — your bank collects the money. The buyer’s bank pays your bank, and you don’t waste nights chasing emails or overdue reminders.

Few Names to Remember in the LC Chain

- Applicant: your buyer, the one asking their bank to open the LC.

- Issuing Bank: their bank, the one making the promise.

- Beneficiary: that’s you, the seller waiting for payment.

- Advising/Confirming Bank: often your own bank, the one that checks the LC and sometimes adds its own guarantee if the buyer’s bank feels too far away.

I’ve heard many MSME owners say, “This sounds like a mountain of paperwork.” It does, the first time. But once you’ve done it once or twice, it feels more like a checklist than a puzzle. The Reserve Bank of India (RBI) allows and regulates these transactions. Globally, the process follows a rulebook called UCP 600. Most bankers know it inside out — you don’t need to memorise it, you just need to follow their guidance and keep your documents clean.

At the end of the day, an LC is not a trick or a luxury. It’s a tool. It tells you: deliver what you promised, hand in the documents as agreed, and you’ll get your money. For an MSME, that kind of certainty is rare — and worth the effort.

Types of Letters of Credit and How Small Businesses Actually Use Them

Every MSME I’ve spoken to thinks of a letter of credit as one fixed thing. But walk into any bank branch, and you’ll realise there are multiple versions — each with its own quirks. The choice isn’t academic. It decides how quickly you see your money and how much risk you carry.

Sight LC – Payment Without Waiting

The simplest one. You present your documents, the bank checks them, and the money lands in your account.

Take the case of a leather exporter from Kanpur. He ships handbags to a French retailer and needs money quickly to pay workers before Diwali. A sight LC fits perfectly — no waiting, no chasing.

Usance LC – Buyer Buys Time, You Buy Certainty

Here, the buyer pays later, but the bank guarantees the amount.

A Rajkot supplier sells engine parts to an auto major. The OEM insists on 60 days’ credit. He agrees, only because the LC assures him the money will eventually come. Without that, he wouldn’t touch the order.

Standby LC – The Safety Net

Think of this one as insurance. It’s triggered only if the buyer defaults.

A Pune IT firm worked with a Middle East client. The owner admitted: “We signed only because the SBLC was in place. Otherwise, the risk was too high.”

Irrevocable LC – No Backtracking

This is the standard now. Once issued, nobody can change terms unless both sides agree.

A Tirupur textile unit exporting T-shirts insisted on this. They’d been burned once before when a buyer backed out. The irrevocable LC gave them confidence to go ahead.

Confirmed LC – Double Guarantee

Sometimes the seller doesn’t fully trust the buyer’s bank. In that case, their own bank adds its guarantee.

A Kolkata tea exporter used this when dealing with a small African retailer. “If their local bank failed, at least my Indian bank would still pay,” he thought.

Transferable or Back-to-Back LC – Passing the Credit Down

Useful when you’re a middleman relying on smaller suppliers.

A Delhi trader handling a big garment order passed the LC down to two Ludhiana units. Without that arrangement, he couldn’t have taken the deal at all.

Red Clause LC – Money Before Shipping

Rare, but powerful. This allows a seller to take part of the money in advance.

One rice exporter from Raipur managed to buy paddy only because of a red clause LC. Otherwise, he would’ve needed a loan at 18% interest.

The real takeaway: these aren’t just banking terms. They’re choices that shape survival. Pick the right one, and you keep cash moving. Pick the wrong one, and you may end up with money tied up for months while still paying suppliers out of pocket.

LC Compliance & Common Pitfalls for MSMEs

Ask any exporter who has used a letter of credit more than once, and you’ll hear a story about a deal gone wrong because of paperwork. The LC protects you, yes — but only if every line in your documents matches what the bank expects. A tiny slip can mean weeks of delay or a penalty that eats into your margin.

Take the case of a Tirupur garment exporter last year. He shipped 5,000 T-shirts to Europe. Everything was fine — until the bank flagged that the invoice said “cotton T-shirt” while the LC wording was “100% cotton T-shirt.” One missing phrase, and payment was held up for 20 days. He had to rush to get an amendment, pay extra charges, and meanwhile his workers waited for salaries.

Another story came from a rice exporter in Raipur. His goods reached the port, but the bill of lading had a typo in the consignee’s address. The overseas bank refused to honour the LC until it was corrected. By the time the correction came, demurrage charges had piled up. The sale was profitable on paper, but by the time he paid the port, he barely broke even.

These mistakes are common because most MSMEs don’t have a dedicated documentation team. Owners are busy running factories or chasing orders, and paperwork becomes an afterthought. But under LC rules — governed globally by UCP 600 and checked locally by your bank — precision matters more than speed.

The most frequent pitfalls are:

- Invoices that don’t match the LC wording word-for-word.

- Insurance policies issued in the wrong currency.

- Shipment dates that slip past the LC deadline.

- Bills of lading with spelling errors or missing signatures.

- Incomplete certificates of origin or inspection.

Fixing these errors isn’t impossible, but it’s costly. Banks charge discrepancy fees, and buyers sometimes use the delay as leverage to renegotiate. For a small firm, that can wipe out weeks of profit.

The best approach is to treat the LC as a checklist, not just a contract. Sit with your bank officer before shipping, line up the required documents, and double-check every field. It feels tedious — but it’s cheaper than watching your payment get stuck in limbo.

Business Outcomes: How LCs Impact MSME Growth

For most MSMEs, the barrier isn’t getting orders. It’s getting paid. Everyone talks about sales; nobody talks about the sleepless nights when payments don’t come on time. That’s where a letter of credit shows its worth.

A parts manufacturer in Rajkot a few years back had never exported, even though buyers asked. His line was always the same: “Too risky, what if they don’t pay?” Then a German buyer offered an irrevocable LC. He shipped. The money came through without delay. That one deal doubled his annual sales.

Closer home, in Morbi, a ceramic unit supplying tiles to a large corporate used to wait months for payment. The owner said cash flow was so tight he once borrowed at 24% interest just to keep furnaces running. After switching to an inland LC, his payments came on time.

This is what an LC does. It doesn’t just protect a transaction. It frees up your working capital. It makes you look serious in the eyes of banks. Once you manage two or three clean LC deals, you’ll find it easier to get ECGC cover, or even discount bills through TReDS without too much questioning. Your banker sees you differently.

And don’t ignore the way things are shifting. A few branches in Mumbai and Delhi are testing eUCP — digital versions of the same old LC paperwork. Early adopters will cut courier delays, save fees, and get cash in hand faster. Right now it’s clunky, but it’s coming.

For a small business, this isn’t theory. It’s survival. An LC gives you room to breathe. It gives you the confidence to take larger orders and the courage to work with new buyers. And in MSME life, that breathing room is everything.

Conclusion

Most MSMEs walk away with the same thought: “The LC looked scary at first, but it saved my business.” That’s really the point. A letter of credit isn’t decoration. It’s a lifeline. It turns risky deals into manageable ones and gives you the confidence to step outside your comfort zone.

If you’re considering your first LC, here’s what to keep in front of you:

MSME Letter of Credit Checklist

- Match every word on your invoice to the LC terms — even small typos can block payment.

- Don’t leave paperwork to the last minute. Sit with your bank officer before shipping.

- If you don’t trust the buyer’s bank, ask for a confirmed LC through your own bank.

- Push back on unnecessary charges. Many banks have special fee slabs for MSMEs.

- If cash is tight, explore red clause or inland LCs to unlock funds faster.

- Keep an eye on new digital pilots like eUCP — they’ll save time once banks roll them out.

An LC won’t solve every problem. You’ll still deal with customs headaches, shipping delays, and buyers who want endless credit. But it takes away the worst risk of all — not getting paid. For a small business owner juggling thin margins, that certainty is priceless.

Empowering MSMEs to grow smarter

Tata nexarc delivers powerful solutions for MSMEs—discover tenders, logistics solutions, and streamline procurement. Everything your business needs, all in one place.

FAQs

Is a letter of credit mandatory for all export orders from India?

How much do Indian banks typically charge MSMEs to issue an LC?

What happens if the buyer refuses to honour an LC after shipment?

Can an LC be used for domestic trade within India, or only for exports?

What documents do Indian MSMEs need to submit for an LC?

How long does it usually take to receive payment under a sight LC?

What is the difference between a letter of credit and invoice factoring for MSMEs?

Does ECGC cover apply when exports are backed by a letter of credit?

Can digital LCs (eUCP) be used by Indian MSMEs in 2025?

What risks remain for MSMEs even when using a confirmed LC?

Ananya Mittal blends a background in data science with a passion for writing, contributing to Tata Nexarc’s efforts in creating insightful, data-informed content for MSMEs. Her work focuses on exploring sector-specific challenges and opportunities across procurement, logistics, and business strategy. She is also involved in leveraging analytics to strengthen content performance and deliver actionable insights to India's growing B2B ecosystem.